By leveraging automated systems, businesses can ensure that all tasks related to closing entries are handled seamlessly, reducing manual effort and minimizing errors. The trial balance is like a snapshot of your business’s financial health at a specific moment. It lists the current balances in all your general ledger accounts. In this case, we can see the snapshot of the opening trial balance below. Manually creating your closing entries can be a tiresome and time-consuming process.

Post navigation

All accounts can be classified as either permanent (real) ortemporary (nominal) (Figure5.3). It’s vital in business to keep a detailed record of your accounts. All accounts can be classified as either permanent (real) or temporary (nominal) (Figure 5.3). Shaun Conrad is a Certified Public Accountant and CPA exam expert with a passion is sales revenue a debit or credit in business for teaching. After almost a decade of experience in public accounting, he created MyAccountingCourse.com to help people learn accounting & finance, pass the CPA exam, and start their career. Instead, as a form of distribution of a firm’s accumulated earnings, dividends are treated as a distribution of equity of the business.

Step 2: Transfer Expenses

- The second part is the date of record that determines who receives the dividends, and the third part is the date of payment, which is the date that payments are made.

- In this article, we will explore how to prepare closing entries in accounting, and provide a step-by-step guide to help you get it right.

- Revenue, expense, and dividend accounts affect retained earnings and are closed so they can accumulate new balances in the next period, which is an application of the time period assumption.

- The business has been operating for several years but does not have the resources for accounting software.

- It also helps the company keep thorough records of account balances affecting retained earnings.

The net result of these activities is to move the net profit or net loss for the period into the retained earnings account, which appears in the stockholders’ equity section of the balance sheet. Remember, dividends are a contra stockholders’ equity account.It is contra to retained earnings. The remaining balance in Retained Earnings is$4,565 (Figure5.6).

Closing entries Closing procedure

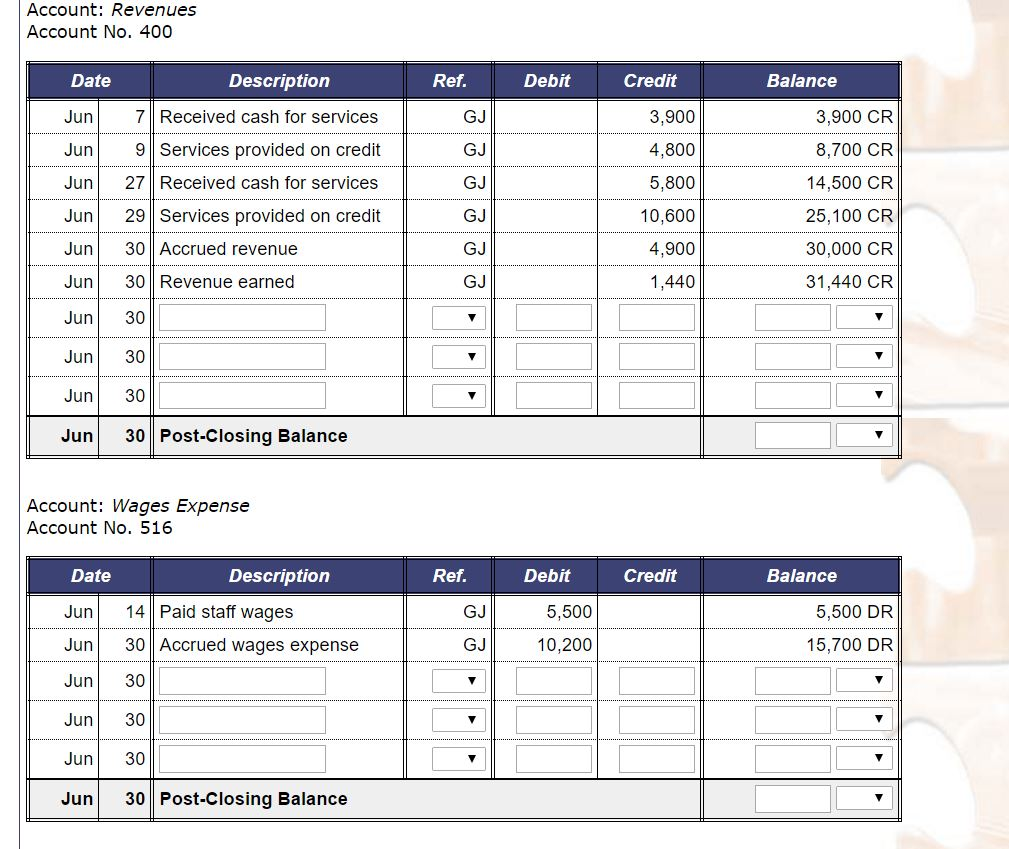

The second entry requires expense accounts close to the Income Summary account. To get a zero balance in an expense account, the entry will show a credit to expenses and a debit to Income Summary. Printing Plus has $100 of supplies expense, $75 of depreciation expense–equipment, $5,100 of salaries expense, and $300 of utility expense, each with a debit balance on the adjusted trial balance. The closing entry will credit Supplies Expense, Depreciation Expense–Equipment, Salaries Expense, and Utility Expense, and debit Income Summary. Closing entries are a fundamental part of accounting, essential for resetting temporary accounts and ensuring accurate financial records for the next period.

Since the income summary account is only a transitional account, it is also acceptable to close directly to the retained earnings account and bypass the income summary account entirely. The $9,000 of expenses generated through the accounting period will be shifted from the income summary to the expense account. The $10,000 of revenue generated through the accounting period will be shifted to the income summary account. In this example, the business will have made $10,000 in revenue over the accounting period.

Step 1: Clear revenue to the income summary account

They are also transparent with their internal trial balances in several key government offices. Check out this article talking about the seminars on the accounting cycle and this public pre-closing trial balance presented by the Philippines Department of Health. Now, all the temporary accounts have their respective figures allocated, showcasing the revenue the bakery has generated, the expenses it has incurred, and the dividends declared throughout the past year. All of Paul’s revenue or income accounts are debited and credited to the income summary account.

The purpose of closing entries is to merge your accounts so you can determine your retained earnings. Retained earnings represent the amount your business owns after paying expenses and dividends for a specific time period. Temporary account balances can be shifted directly to the retained earnings account or an intermediate account known as the income summary account. All of these entries have emptied the revenue, expense, and income summary accounts, and shifted the net profit for the period to the retained earnings account. Only incomestatement accounts help us summarize income, so only incomestatement accounts should go into income summary. Our discussion here begins with journalizing and posting theclosing entries (Figure5.2).

The balances from these temporary accounts have been transferred to the permanent account, retained earnings. Temporary accounts are income statement accounts that are used to track accounting activity during an accounting period. For example, the revenues account records the amount of revenues earned during an accounting period—not during the life of the company. We don’t want the 2015 revenue account to show 2014 revenue numbers.

The next day, January 1, 2019, you get ready for work, but before you go to the office, you decide to review your financials for 2019. What are your total expenses for rent, electricity, cable and internet, gas, and food for the current year? You have also not incurred any expenses yet for rent, electricity, cable, internet, gas or food. This means that the current balance of these accounts is zero, because they were closed on December 31, 2018, to complete the annual accounting period. After the closing journal entry, the balance on the dividend account is zero, and the retained earnings account has been reduced by 200.

Net income is the portion of gross income that’s left over after all expenses have been met. The term can also mean whatever they receive in their paycheck after taxes have been withheld. Chartered accountant Michael Brown is the founder and CEO of Double Entry Bookkeeping.